How Your Credit Score Influences Your Auto Loan Rate

[ad_1]

The most significant element of an auto-financial loan is arguably the fascination amount. It specifically influences the dimension of month to month payments and all round loan tenor. Interest charges can even engage in a job in the closing getting determination, potent adequate to override sentimental invest in causes this sort of as brand name loyalty. It goes devoid of saying, thus, that possible car or truck consumers fork out focus to things that decide their interest rates when procuring for vehicle-financing solutions.

One of this kind of elements is the credit rating rating. It is in essence a weighted rating that tells vehicle-loan providers how considerably possibility they are getting on by working with a prospective borrower. You most most likely have a credit report if you have any credit accounts, this sort of as credit rating playing cards, mortgages or financial loans. This report then forms the foundation for pinpointing your credit score rating.

It is not an specific measure, but it does shed gentle on aspects such as the borrower’s willingness and ability to provider the mortgage. Merely set, the greater your credit history score, the greater your chances of securing an car loan with favourable interest charges. This is significantly essential nowadays as we navigate the period of curiosity price hikes and inflationary pressures.

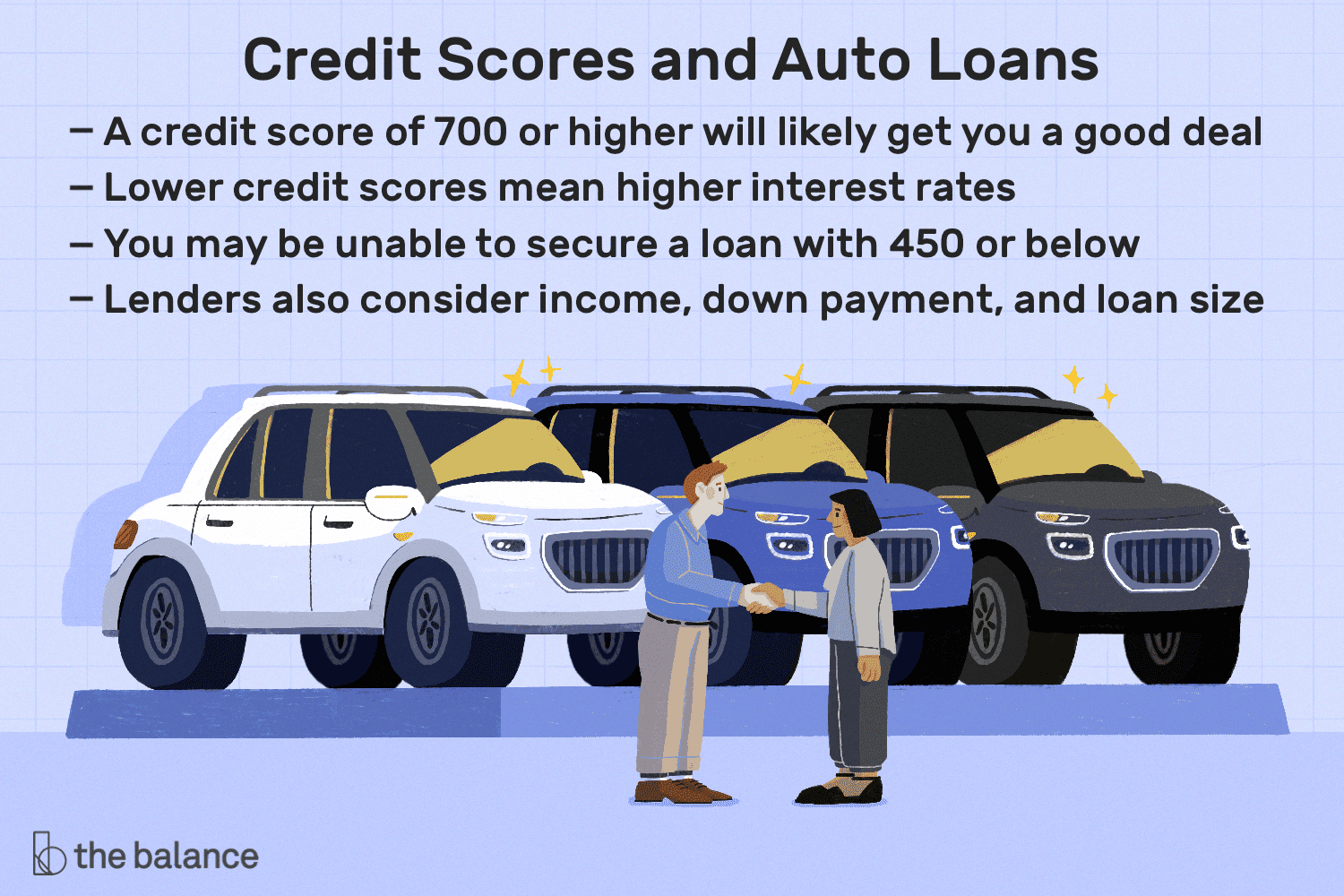

Using your credit history rating to protected the most effective desire fees

By means of Experian

The total reason of the credit history rating is common. However, distinct loan providers in distinctive components of the entire world have their possess requirements to measure an individual’s creditworthiness. When you implement for an auto personal loan in the US, the financial institution will operate a credit rating look at as part of the method. The greater part of the lending establishments use FICO credit score scores. This is a 3-digit rating assigned to a borrower immediately after the credit rating check out physical exercise.

It was to begin with designed in 1989 by a details analytics firm known as Reasonable Isaac Corporation. Nowadays, there are quite a few variations of the FICO algorithm (and other scoring versions, for that make any difference), but they are all aimed at ascertaining the borrower’s skill to consider on credit score.

By means of The Harmony

In accordance to the CFPB (Customer Monetary Defense Bureau) Shopper Credit score Panel, there are 5 distinct borrower profiles sorted into the pursuing credit score score buckets: Tremendous-primary (720 & higher than) Key (660-719) In close proximity to-key (620-659) Subprime (580-619) Deep subprime (underneath 580). A borrower with a score down below 660 can however protected car financial loans, but they will be far more pricey than a Key or Super-key borrower with a score north of 661. The logic in this article is that you will want to retain your credit history score as superior as possible to get the ideal deals when procuring for automobile loans.

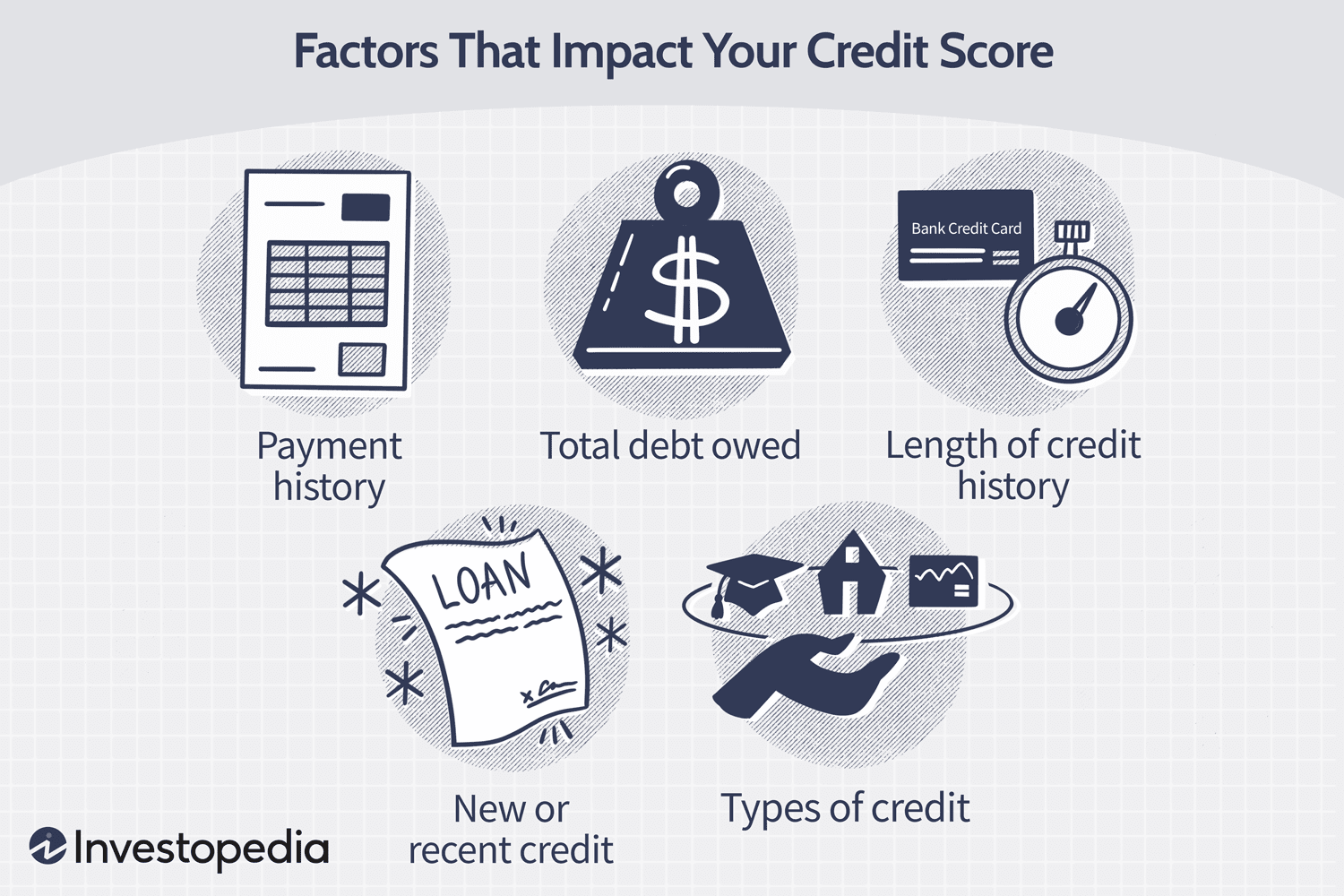

Things that damage your credit score rating

By using Investopedia

An exceptional credit rating is the end result of watchful and deliberate organizing, and being aware of the potential pitfalls can enable the borrower stay away from making missteps that pull down the rating into unwelcome territory.

Producing a late payment

Payment heritage on your credit score obligations accounts for up to 35% of the FICO score. In accordance to FICO, a payment that is 30 times late can charge somebody with a credit rating rating of 780 or increased anywhere from 90 to 110 points. It is significant to make payments as at when owing and proactively get to out to the loan company if, for any cause, payment will be delayed.

A substantial credit card debt-to-credit rating utilization ratio

Credit rating record is crafted by a consistent cycle of credit score utilization and fork out downs. Nonetheless, you will want to keep an eye on the proportion of your financial debt load to over-all credit score. The lessen your balances relative to your whole offered credit score, the far better your score will be.

Non-utilization of credit

On the other hand, no credit historical past for an prolonged period of time can also adversely affect the borrower’s credit rating rating. Loan providers and creditors have absolutely nothing to report to credit history bureaus when you do not employ your credit score accounts. This would make it far more difficult to assess foreseeable future loan purposes.

Personal bankruptcy

Submitting for bankruptcy has a person of the most considerable impacts on your credit rating rating. It can wipe as considerably as 240 factors from an individual’s score, and what is far more? A individual bankruptcy report can stay on the credit background for up to ten several years.

This listing is by no implies exhaustive, and other factors this sort of as frequency of credit history programs, credit card closure, cost-offs and refinancing all influence credit rating scores in varying levels.

Bettering your credit rating

Improving upon your credit score rating will entail keeping away from the pitfalls earlier discovered previously mentioned. Tactics this kind of as prompt and typical bill payments, keeping a small credit card debt-to-credit history utilization ratio (preferably about 30%), retaining credit rating card accounts open up and staying away from a number of personal loan programs at the moment are all measures in the proper course.

Having said that, even with all these ‘building blocks’ in location, a terrific credit score is not instantaneous. It may possibly take a while to see any enhancement, specifically given that adverse experiences can stay on your credit rating record for several years. There is no rigid time frame for credit score development as each and every person’s money scenario is one of a kind. In accordance to Forbes, it could just take wherever from a thirty day period to as much as 10 a long time. Certainly, this is motivated by variables these kinds of as the individual’s recent credit rating position and sum of total publicity.

Securing car loans no matter of credit score rating

Via Geotab

A higher credit score will unquestionably make improvements to your likelihood of securing auto financing and locking up the ideal desire rates. Nonetheless, it’s not all doom-and-gloom for future car or truck potential buyers with weak scores as they are not fully without selections.

No matter of your credit rating rating, searching all-around and contemplating the various funding alternatives is extremely suggested. It is just like browsing for the motor vehicle by itself an typical customer will appraise distinct dealerships and negotiate vigorously prior to making the final decision.

Financial institutions are the conventional sources for obtaining a mortgage, but you may be proscribing your solutions if they are your only thing to consider. Really don’t disregard choice lenders. Doing work with third-occasion funding corporations, these as acquiring your vehicle bank loan by using LoanCenter.com, may possibly deliver you with favourable interest prices or funding terms.

It is crucial to note that simply just acquiring vehicle-personal loan preapprovals (unique from precise mortgage programs) when purchasing about will not influence your credit history rating considering that most scoring models do not take care of this as a tough enquiry.

In summary, a weak credit rating rating may possibly push the cheapest desire rates out of access. Even so, getting a number of selections will strengthen your probabilities of discovering a offer with an interest fee that fits inside your budget and let you to obtain your wished-for auto.

[ad_2]

Resource link

.jpg "Quarry Operations: Extreme Duty Lubrication for Rock Processing Equipment")