Mainland Chinese Truck Market Remains Bearish with Supply Chain Shocks

[ad_1]

Mainland Chinese medium- and hefty-obligation vans (MHDTs) have

entered a bear market considering that mid-2021. Despite the fact that the market staged a

slight restoration following the easing of power shortages and

injection of plan stimulus from late last 12 months, unpredicted

headwinds brought by the Russia-Ukraine disaster and domestic Omicron

outbreak plunged the marketplace back into weak point in the 2nd

quarter of 2022. Amid pandemic-induced lockdowns in Jilin and

Shanghai, generation of MHDT hit the lowest reading for April about

a 10 years. In our May possibly forecast, we downgraded the mainland Chinese

MHDT generation for 2022 by 5% to 1.13 million units, a drop of

23% in comparison with 2021.

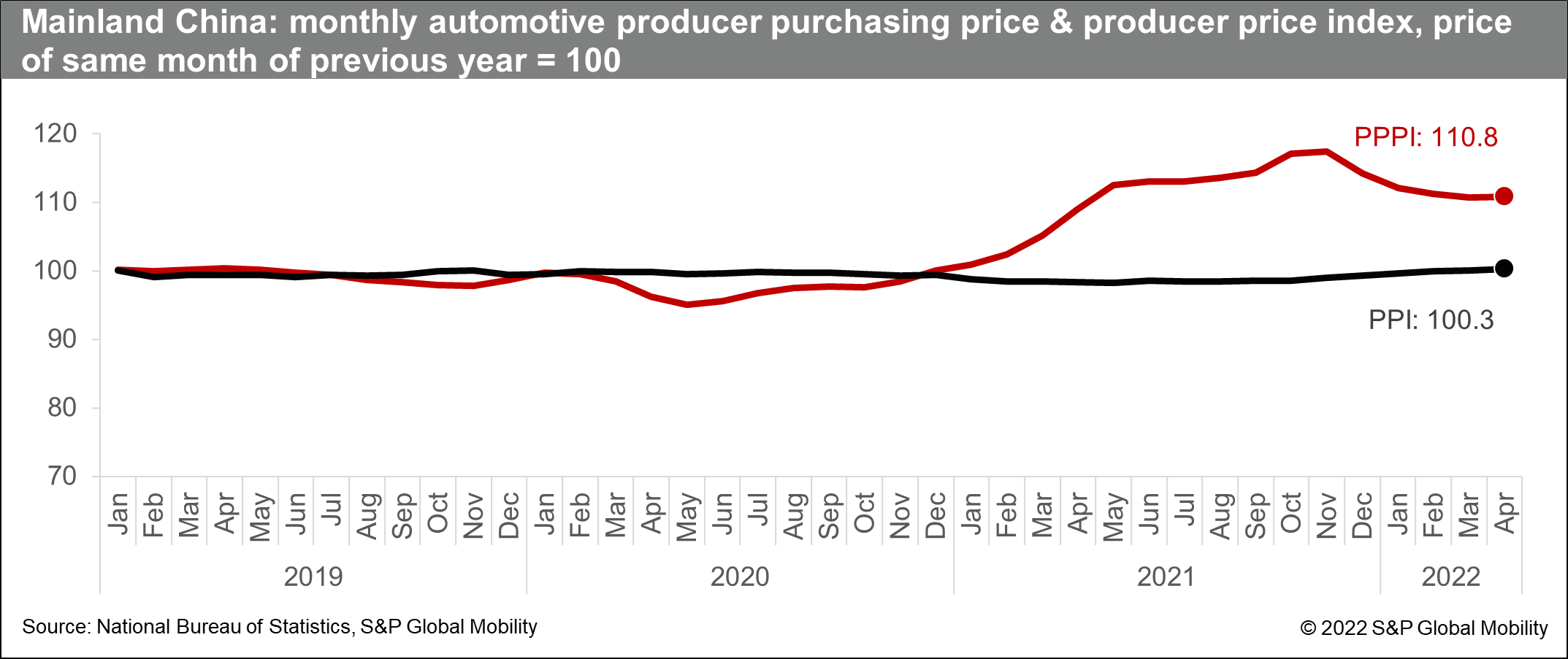

Exterior geopolitical tensions drive up producer charges

As uncooked resources stand for 20-30% of the price of creation for

hefty vehicles, raw material expenses partly determine the

profitability of truck producers. Owing to the international economic

restoration from the COVID-19 scare, commodity prices have

gone through an upcycle due to the fact late 2020. The rally obtained extra steam

in the 1st quarter of 2022 with the outbreak of the

Russia-Ukraine war. Specifically, the cold-rolled metal price that

accounts for about 60% of the complete uncooked substance prices for a large

truck surged by 3% in March 2022 from the stage of January,

expanding the advancement to much more than 40% as in comparison to the similar

time period of 2020. Also, the diesel cost elevated by 15% and passed the

RMB9,000 per metric ton mark by way of January-March 2022. In

distinction, the movement of selling selling prices for significant vans were being

somewhat flat under slack demand from customers, as fuel rate inflation elevated

the operating charges although oversupplied trucking constrained freight

fee progress. As a outcome, the truck producers’ purchasing and

offering price ranges logged major differentiation, in spite of an

increase in selling price of CN6-degree products. This kind of weak inflation

move-as a result of impact has made truck makers to bear the brunt of the

profit margin squeeze particularly following dumping of CN5-amount trucks.

With the Russia-Ukraine disaster envisioned to deepen into 2023,

brief-time period truck generation is as a result lower by all around 25,000 units

in the May outlook.

Inner pandemic resurgences exacerbate provide chain

disruptions

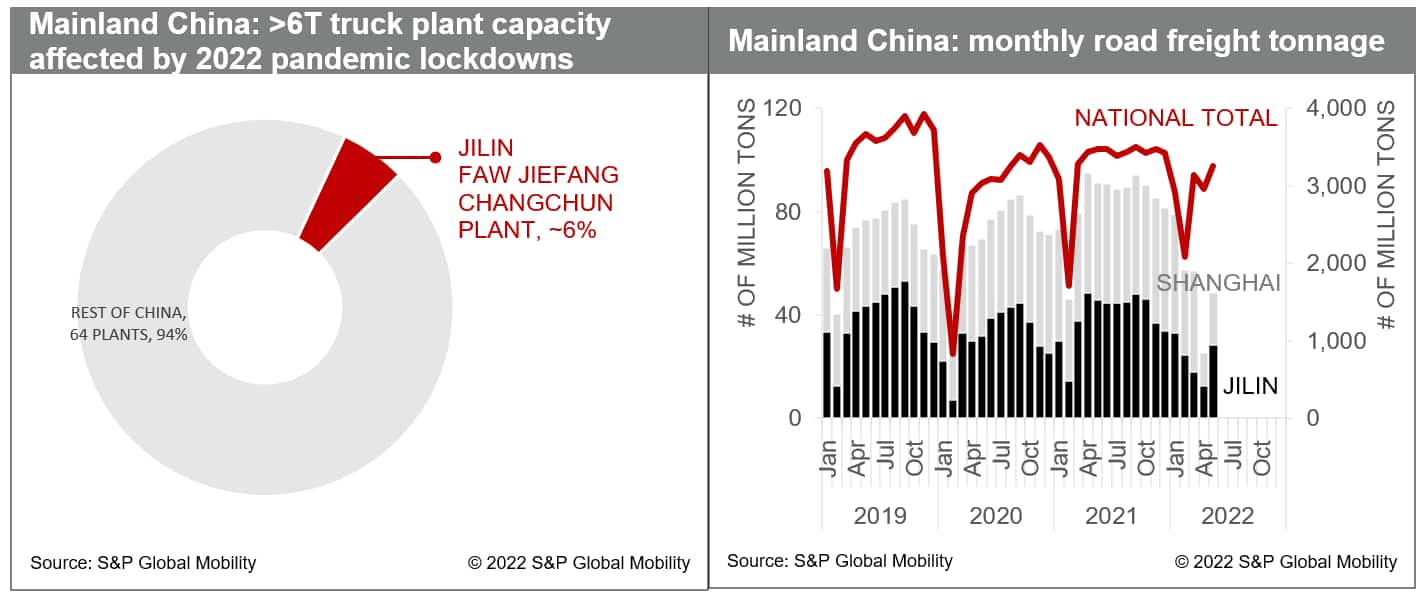

The Omicron wave had triggered massive lockdowns in Jilin

Province (March 11-April 28), Shenzhen Metropolis (March 14-20), and

Shanghai City (March 28-May perhaps 31) considering the fact that March 2022, ensuing in

prevalent business disruptions and logistics snarls. Though

there are couple MHDT producers in the epicenters of the pandemic,

Changchun City and Shanghai Metropolis host about 40 major offer bases

serving main components to mainstream products masking over 90% of

truck generation. Starting off from mid-April, FAW Jiefang’s Changchun

plant and most suppliers managed to resume do the job in the shut-loop

system, but labor shortages less than the mobility manage disabled

them to functionality at regular potential. Meanwhile, demanding

containment measures such as website traffic limitations, nucleic acid

check and quarantine needs, as properly as closure of toll

stations pent up street freight desire and brought on wider repercussions

of component shortages, which in turn dampening truck output.

Beneath the circumstances, the complete reduction of MHDT output in the

second quarter is estimated to reach 100,000 models. With ramping up

attempts to easy logistics and restore organization, the function

resumption fee of enterprises over specified sizing in Shanghai

City enhanced to 96% by mid-June and will completely recover from July.

Coupled with expansionary policies and ample ability

reserves, these could assist MHDT output to decide up and offset

the pandemic-induced reduction in the second 50 %.

A even more downgrade to outlook is underneath evaluation, as the

government’s reliance on the “dynamic zero-COVID” approach and

cash outflows led by the Fed’s tightened cycle are possible to

weaken organization sentiment and subdue demand recovery. On the other

hand, the rebuilding of supplier inventories of CN6-stage MHDTs

climbed from 280,000 models in early this year to 380,000 models by

April, way higher than the common fees of 150,000-170,000 models.

Moreover, there ended up additional than 70,000 models CN5-stage new

vehicles (bought as employed vehicles) remaining in the market, exacerbating

de-stocking pressures.

This posting was printed by S&P International Mobility and not by S&P Worldwide Rankings, which is a separately managed division of S&P International.

[ad_2]

Supply connection